If the last few years have shown us anything, it’s that we must be ready for the unexpected. From the disruptions of the global pandemic to soaring inflation, from political scandals to a war of aggression in Ukraine—life as we know it is changing.

The public sector doesn’t exist in a vacuum. Global events have a direct effect on national public services, and uncertainty causes disruption. The public sector must adapt to these changes if it is to continue delivering essential services for the taxpayer. Long-term funding challenges, climate change, and changing demographics also add to the pressures the global public sector is facing, and with technology changing the way we work, how does the role of internal audit fit into this complex web of demands and transformations?

As organizations react to these external changes, their assurance needs will inevitably change too. If internal audit is to stay relevant, it needs to keep pace with the changing demands of the organization.

To get a better understanding of how to improve the impact of internal audit and unlock its full potential, Chartered Institute of Public Finance and Accountancy (CIPFA) asked over 800 internal audit professionals and clients from across the United Kingdom for their experiences and views. This research forms the basis of our major report Internal audit: untapped potential. We wanted to build a snapshot of the current state of internal audit and identify where it’s already making an impact. We also wanted to explore how it can stay relevant to clients while continuing to deliver value for the taxpayer.

Our research revealed that 93 percent of the internal audit leaders who responded strongly agreed that internal audit supports the management of the organization, while 88 percent of managers who responded felt the same. Although there is some disparity between the two figures, they show that managers and heads of internal audit broadly agree that internal audit contributes to effective organizational management. Despite these promising statistics, when asked questions about the specific areas where internal audit is making an impact, there was significant disagreement.

Divergent Views

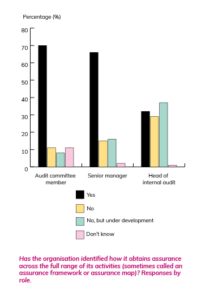

We found that heads of internal audit and their clients, the management of organizations, often had substantially different views on what internal audit currently delivers to the organization. For example, 73 percent of heads of internal audit believe that they act as an independent critical friend on committees or steering groups, with just 43 percent of management agreeing with this. More worryisome, only 35 percent of audit committee members thought that internal audit provided this role. Ninety-one per cent of internal audit leaders said they provide advice on new systems and developments, but only 62 percent of managers agreed. This disparity is common across a range of different services and roles provided by internal audit, with clients consistently believing internal audit’s input is significantly less than what the heads of internal audit believe.

This shows that heads of internal audit need to be more vocal about the work their teams are actually doing for the organization. They need to become advocates for internal audit and promote the work of their teams, while clearly explaining to management how vital internal audit is and how it can help the organization reach its goals. Only then will the input of audit teams be fully understood and appreciated by clients, managers, and audit committees.

This shows that heads of internal audit need to be more vocal about the work their teams are actually doing for the organization. They need to become advocates for internal audit and promote the work of their teams, while clearly explaining to management how vital internal audit is and how it can help the organization reach its goals. Only then will the input of audit teams be fully understood and appreciated by clients, managers, and audit committees.

The more management understands the role of internal audit, the more expectations they will have of it. Higher expectations means that internal audit becomes more intrinsically valuable and more relevant to an organization, ensuring its important role in the future.

Three Areas of Focus

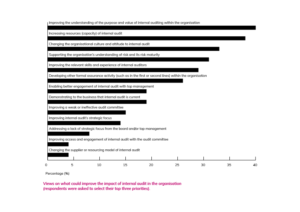

More strategic coverage can also help internal audit transform and adapt for an uncertain future. We asked respondents to identify three key areas that internal audit should focus on in the future to have the greatest impact on an organization. Cybersecurity was the top priority, with just under 60 percent of respondents wanting internal audit to focus on this key strategic area in the next three years. Just over 50 percent identified digitization and data use within organizations as the next most important area, while 47 percent thought that climate change and sustainability would be important areas of focus for internal audit professionals in the next three years.

The area of internal financial risk, which internal audit has traditionally provided assurance in, such as payroll and income, are generally already well managed with little exposure to risk. So, does internal audit still have a role to play in mitigating financial risk? About one-third (35 percent) of respondents said they thought financial viability was a key area for the future. This includes more strategic areas such as financial resilience and medium- and long-term financial strategies—both of which carry considerable risk to the organization. Without seeking to influence the financial policies themselves, internal audit can provide vital independent assurance to decision makers to allow them to take on more risk and be more ambitious.

If internal audit takes a more strategic role in emerging issues and provides assurance not just around internal financial risk, then it can position itself as a trusted partner to the organization. In the coming years, it will be vital for audit professionals to keep up with the changing demands of clients, and the world around us, if internal audit is to stay relevant.

The Skills Gap

Continual life-long learning is also essential if internal audit is to stay on the front foot. It is this up-skilling that will help auditors keep pace with emerging organizational demands, like cloud computing and cyber security. Out of the heads of internal auditors who responded to our survey, 55 percent agreed that they had sufficient skills and experience to meet the needs of the organization. This is broadly similar to the number of senior managers who agreed that their internal audit teams had the skills needed. There is still room for improvement in this area.

In its 2020 report on the future of jobs, the World Economic Forum identified some key technologies that companies thought would most likely be adopted by 2025. Cloud computing, big data analysis, artificial intelligence, and cybersecurity all came out on top. These represent growth areas for internal audit and where internal audit professionals will have to upskill to provide maximum value to the organization.

Internal auditors cannot be subject matter experts in all these areas, of course, and some aspects will have to be outsourced to specialized firms. Internal auditors can, however, oversee the organization’s direction and approach to these key strategic areas, provide independent assurance and act as a critical friend where necessary. Having good communication, critical and analytical reasoning skills, financial literacy, as well as risk-based auditing skills will help internal auditors tackle these complex subject areas.

Internal audit can have a bright future. Although the world is in a particularly uncertain phase, and organizations’ assurance requirements are rapidly changing to reflect this, internal audit can still make a significant impact and provide a valuable service. But to do this, it must also adapt.

Internal audit can have a bright future. Although the world is in a particularly uncertain phase, and organizations’ assurance requirements are rapidly changing to reflect this, internal audit can still make a significant impact and provide a valuable service. But to do this, it must also adapt.

Embracing New Challenges

To stay still is to move backwards when the pace of change is so considerable. Internal audit’s future lies in embracing new challenges such as cybersecurity, financial viability, climate change, artificial intelligence and big data. It can provide organizations with the assurance they so badly need around these issues – allowing them to embrace new technologies and ambitious strategies. To do this, internal auditors need access to learning and development to equip them with appropriate skills to find solutions to these complex issues.

All of this, however, will not lead to the wanted outcomes if heads of internal audit do not advocate and promote the work of their teams within organizations. They must make sure management and clients understand their assurance needs and how internal audit teams support organizations to reach their goals.

Good public financial management is at the core of delivering value for money and improving public services. A much broader, more diverse, and louder internal audit function can reinforce and support good financial management, both now and well into the future. ![]()

![]()

Khalid Hamid is International Director of the Chartered Institute of Public Finance and Accountancy.