The coronavirus crisis has upended all areas of corporate America and its effects are likely to linger long after the pandemic has passed. A new study indicates that the internal audit profession is no exception and is undergoing some vast changes, due to the current crisis.

According to a survey from the Institute of Internal Audit’s Audit Executive Center, internal audit budgets are likely to decline, risk assessments will become more frequent, audit processes are changing, and audit leaders are looking for different skill sets in those they hire.

The survey, conducted in early June with response from 486 chief audit executives (CAEs) and directors from the United States and Canada, examined the effects of COVID-19 on topics such as internal audit budgets and the frequency of risk assessments, helping frame a view of the expectations for the next 12 months.

Declining Budgets

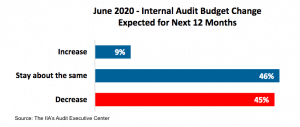

Despite COVID-19 introducing new risks, internal audit budgets are likely to decline at most shops during the next 12 months, according to the survey. Nearly half, (45 percent) of respondents anticipate cuts to their budgets and 46 percent say they will see no change. That outcome would reverse a trend toward increasing budgets. Over the previous 12 months, 37 percent of internal audit leaders said budgets had increased, compared to just 9 percent who expect budgets to rise in the next year.

Not surprisingly, the deepest cuts are likely to come to travel budgets. Nearly two-thirds of respondents expect a “significant decrease” to travel funds and another 22 percent expect more modest cuts. With so much uncertainty about how long the crisis will last, internal auditors are becoming more acclimated to remote audit work. They are also getting more creative about using video platforms to conduct meetings and even to observe processes and other work remotely to conduct audits from afar. Some of those practices may continue after COVID-19.

Not surprisingly, the deepest cuts are likely to come to travel budgets. Nearly two-thirds of respondents expect a “significant decrease” to travel funds and another 22 percent expect more modest cuts. With so much uncertainty about how long the crisis will last, internal auditors are becoming more acclimated to remote audit work. They are also getting more creative about using video platforms to conduct meetings and even to observe processes and other work remotely to conduct audits from afar. Some of those practices may continue after COVID-19.

Compared to the overwhelming decrease in travel budgets, internal staffing budgets have experienced less of a hit. Only 6 percent of respondents say that hiring budgets will significantly decrease and 21 percent say that the budget would slightly decrease. Among industries, the impact is being felt differently as well, with educational services and consumer-facing industries expecting the greatest cuts to internal staffing budgets.

For external sourcing expectations, the number of respondents who expected significant decreases (16 percent) was the same as the number who expected increases (17 percent). The polarity may reflect different needs of different industries in addressing new risks brought on by the pandemic and a need for external talent to address new demands.

Overall, the industries facing the most budget cuts are in educational services and manufacturing, while financial services and insurance are relatively unaffected, with only one-third of industry leaders saying they expect budget cuts. In education, public administration, health care and social assistance, and consumer facing industries, about one in four of respondents expect significant cuts to their budgets, while only one in 17 respondents in finance and insurance expect significant cuts to their budgets.

More Frequent Risk Assessments

The pandemic has exposed the problem with the annual risk assessment and audit planning cycle. Most CAEs have had to ditch the annual plan and reassess how the risk landscape has changed in light of the crisis. To adjust to expectations, internal audit leaders across all industries plan on increasing the frequency of risk assessments. In the consumer-facing sector, where coronavirus has imparted the greatest toll, 32 percent of respondents expect significant increases in the frequency of risk assessments and 40 percent expect slight increases.

Internal audit leaders are also updating their audit plans more frequently. More than 60 percent of respondents said that there would be updating the internal audit plan more often. Internal audit teams recognize the uncertainty that COVID-19 brings and is prepared to constantly reassess and readjust to the new situations, indicating a flexibility and proactiveness within internal audit.

Changing Audit Processes

The most prominent change that COVID-19 has introduced to internal audit functions is the need for remote work. With many offices still closed, 80 percent of respondents anticipate a continuation in auditors working from home during the next 12 months and 71 percent anticipate decreased time spent on site. To adjust to these changes, 73 percent anticipate more flexible audit plans to better adjust to the ever-changing circumstances.

In addition, 49 percent of respondents anticipate greater uses of data analytics and 39 percent anticipate more usage of agile auditing techniques. Less anticipated processes include more use of audit software, more investment in automation, and more use of robotic process automation. With many audit leaders projecting smaller budgets, it remains to be seen if these investments will materialize.

Evolving Skill Sets

While CAEs always say they are seeking internal audit candidates with excellent communication and analytic skills, those competencies are in even greater demand due to the pandemic. The skills most sought after as a result of COVID-19, say respondents, are a mixture of soft skills and analytical skills.

Communication skills topped the chart, with 27 percent expecting a “significant increase” in the demand for candidates with such abilities, and 45 percent expecting a slight increase in demand. The focus on communication skills likely stems from the need for those who can better communicate remotely. Internal audit candidates with cybersecurity, risk management, and data analytics experience are also expected to be in high demand. Roughly 60 to 70 percent of survey respondents acknowledged an increased need for such skills during the next 12 months.

With the crisis mode giving way to the “new normal,” internal auditors need to adjust to the new reality and weather the economic fallout that the virus has brought. With widespread budget cuts anticipated, internal auditors must prioritize what’s important and learn to efficiently and effectively work under new expectations. Remote work situations don’t look to be ending anytime soon. The survey shows that internal audit leaders are preparing to adjust expectations and act proactively in responding to the impacts of the Coronavirus Crisis. ![]()

![]()

Stephanie Liu is assistant editor at Internal Audit 360°