The increasing number of organizational failures in government and non-government sectors have resulted in major reforms in corporate governance codes and practices worldwide. The reforms, such as the Sarbanes Oxley Act in 2002 and The Cadbury Report in 1992, focused mainly on enhancing transparency, accountability, and responsibility at various organizational levels. It also led to significant changes in traditional monitoring functions, including compliance, risk management, and internal audit.

Governments play a crucial role in promoting good governance practices and accountability by implementing a robust internal audit methodology themselves that positively impacts and enhances the maturity level of the internal audit practices. Internal audit functions’ maturity and effectiveness vary depending on many factors, including internal or external factors, which ultimately impact the overall quality of the internal audit function. Similarly, internal audit quality affects the ability to provide board directors and audit committee members with the required assurance and provide them and the management with insights that add value to the organization.

At the same time, the role of the government could be damaging and might result in restrictions and impairments to the role of internal auditors. In November 2021, the Institute of Internal Auditors (IIA) announced it issued letters to Greece’s Prime Minister and Ministry of Development and Investments, objecting to a last-minute legislative amendment that would infringe on its international standards and code of ethics and the efficient practice of internal auditing. A great action from the IIA global, which we rarely heard about in the past, emphasizes the essential role governments should play in enhancing the internal audit profession.

This article is based on a study that analyzed the impact of the government internal audit methodology on the internal audit quality in non-government entities, especially in countries where governance systems are immature or struggling to improve the oversight functions in non-public sectors.

A Role for Government

Recent corporate governance studies demonstrate that country-level factors influence governance practices much more than firm or industry-level factors. Other studies in the field of corporate governance demonstrate that governments need to get it right first before expecting corporate citizenry to do the right thing. Such research results reinforce governments’ role in promoting good governance practices and accountability, including implementing a robust government internal audit methodology that can positively impact audit practices.

Such a topic is essential, particularly in the developing countries, where some studies suggest that while these countries have introduced reforms to the internal functions, more needs to be done. The government internal audit methodology usually includes regulations, policies and standards for the planning, performance, and reporting of audit work and high-level procedures intended to assist internal audit staff in discharging their duties. It also includes internal audit responsibility, authority, accountability, and policies to achieve consistency in audit activities, standardize the IA and risk assessment approach, and expedite internal audit staff training and development.

Internal Audit Quality Explained

The Institute of Internal Auditors (IIA) has promulgated authoritative guidance contained in its International Professional Practices Framework (IPPF), affirming that an internal audit activity must be designed to add value and improve an organization’s operations. To support the proper design and effective functioning of internal audit operations, the IPPF’s mandatory guidance as outlined in Standard 1300 “Quality Assurance and Improvement Program (QAIP)” requires a Chief Audit Executive (CAE) to develop and maintain a QAIP involving all aspects of the internal audit activity.

The QAIP focuses on assessing the internal audit function’s conformance with the Definition of Internal Auditing, the Core Principles, the IIA Standards, and the IIA Code of Ethics. As per the Quality Assessment Manual of the IIA, the internal audit quality is grouped into four main categories: IA Governance, IA Staff, IA Management, and IA Processes. The IA Governance includes the IA function’s purpose, authority, and responsibility and is focused on maintaining quality around the audit committee activities, charters, governance structure, IA strategy, independence, authority, responsibility, and the QAIP framework.

Also, the IA staff category includes the quality aspects around the internal audit function’s reporting lines, competency, skills structure, resourcing, training, and stakeholder reporting. Furthermore, the IA Management includes the IA methodology, IA policies, IA risk assessment and planning, organizational relationships, stakeholder feedback, IA KPIs, and technology utilization. Finally, the IA Processes category includes the quality of the IA planning documentation, engagement working papers, supporting documents, IA reports, overall opinions, and follow-up on implementing the IA recommendations. In a survey conducted by the Internal Audit Foundation in 2014, survey respondents cited the primary reasons for investing in the quality of the IA function: 1) to identify areas for improvement 2) to increase the credibility of the IA activity within the organization, and 3) to anticipate, meet, or exceed stakeholder expectations.

A Neglected Factor Impacting Internal Audit Quality

Studies in the field of internal audit have highlighted different factors that can impact the quality of the function, including internal auditors’ competency, which significantly impacts internal audit effectiveness. Furthermore, internal audit department size, relationships between internal auditors and external auditors, the level of management support for internal audit performance also directly affect quality. In addition, the audit committee’s involvement in internal audit activities influences IA professionalization and the independence of the IA function is considered a critical factor that impacts IA quality.

However, one of the factors that are not usually considered a major contributing factor is the robustness, level of details, and quality of the government internal audit methodology, which reflect the seriousness of governments in empowering internal audit as a critical governance pillar in the public and non-public sectors.

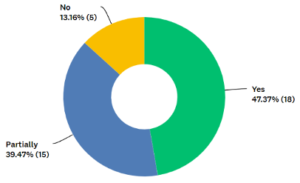

A questionnaire was designed to collect data from more than 75 internal auditors in developing countries about their perceptions which answer central questions, including their level of awareness about the government internal audit methodology and their understanding of the contributing factors that influence the implementation of the government internal audit methodology in non-government entities. As illustrated in the Figure at left, the majority of respondents believes that there is a full (47 percent) or partial (39 percent) positive correlation between the robustness of the government internal audit methodology and internal audit regulations and the maturity level of the internal audit quality in non-government entities.

A questionnaire was designed to collect data from more than 75 internal auditors in developing countries about their perceptions which answer central questions, including their level of awareness about the government internal audit methodology and their understanding of the contributing factors that influence the implementation of the government internal audit methodology in non-government entities. As illustrated in the Figure at left, the majority of respondents believes that there is a full (47 percent) or partial (39 percent) positive correlation between the robustness of the government internal audit methodology and internal audit regulations and the maturity level of the internal audit quality in non-government entities.

Internal Auditors Perception on the Impact of Government IA Methodology on IA Practices in Non-Government Entities

A questionnaire was designed to collect data from more than 75 internal auditors in developing countries about their perceptions which answer four central questions, including their level of awareness about the government IA methodology and their understanding of the contributing factors that influence the implementation of the government IA methodology in non-government entities. It also aimed to understand the contributing factors that influence the adoption of the government IA methodology by non-government entities. Furthermore, it aimed to understand the internal auditors’ perception of the impact of the government IA methodology on the four categories of IA quality in non-government entities: IA governance, IA staff, IA management, and IA processes.

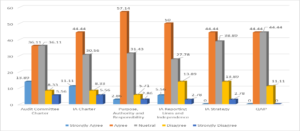

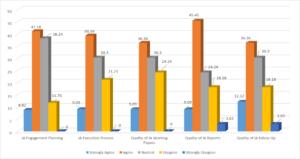

This study assumes that the robustness, level of details, and quality of the government IA methodology are significant factors that reflect the seriousness of governments in empowering IA as a critical governance pillar in the public and non-public sectors. The impact of the government IA methodology on the different aspects of the IA governance quality category in the non-government entities is summarized in the graph below:

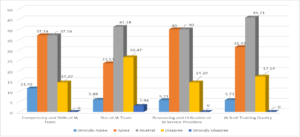

The impact of the government IA methodology on the different aspects of the IA staff quality category in the non-government entities is summarized in the graph below:

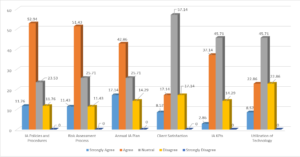

The impact of the government IA methodology on the different aspects of the IA management quality category in the non-government entities is summarized in the graph below:

The impact of the government IA methodology on the different aspects of the IA processes quality category in the non-government entities is summarized in the graph below:

The Link Between Government IA and Non-Government IA

The study has analyzed the impact of the government internal audit methodology on the internal audit quality in non-government entities. It is clear that the level of attention that the government provides to its own internal audit methodology plays a significant role in the seriousness of the business community in adopting internal audit best practices. As a result of the questionnaire data analysis, it is evident that there is a strong relationship between the robustness of the government IA methodology and the IA quality in the non-government entities. In the case where the government IA methodology is robust, the positive impact on the four IA quality aspects was evident, especially with regards to the IA quality factors that are not affected by internal factors or budget restrictions, such as IA charters, policies, IA staff competencies, IA processes, IA planning, and risk assessment. However, the impact was less in terms of the IA quality aspects impacted by internal factors, such as client satisfaction, quality of training, utilization of service providers, IA KPIs, and utilization of technology.

In addition, the quality of communication of the government IA methodology and the government’s seriousness in the implementation of the government IA methodology have a positive impact on the level of the voluntary adoption of the methodology by the IA departments in the non-government entities. On the other hand, awareness about the government IA methodology is low in the case of a weak government IA methodology. In other words, even if the government IA methodology is weak, it will still impact the IA quality in the non-government entities. However, the impact will reflect the same level of quality of the government IA methodology, which is negative in the case of a weak government IA methodology.

The Way Forward

The implications of such findings are highly significant for governments trying to find ways to improve governance and accountability across the different sectors. The findings suggest that governments should design a robust IA framework and methodology, communicate it to the relevant stakeholders, and show seriousness in the follow-up on the implementation of the methodology to improve the overall maturity and quality of the IA practices in the country. One of the successful examples is the Abu Dhabi Accountability Authority (ADAA) that has put a leading IA methodology in place, which was introduced in 2010 based on the international internal audit standards and global best practices. Such examples need to be studied and analyzed by developing countries in order to elevate the internal audit practices across the public and non-public sectors, which will enhance the overall maturity of the governance practices in these countries. ![]()

![]()

Ehab Saif, MSc, CMA, CIA, CFE, is a specialist in internal audit, risk management, and governance, based in Abu Dhabi, United Arab Emirates.

Good article