Main barriers for internal audit to advance in adoption of key technologies:

- Talent Gaps: Internal audit functions just can’t find enough people with the right skills to enable implantation of advanced technologies.

- Complacency: Internal audit suffers somewhat from tech myopia, remaining cautious in trying new things and maintaining a “that’s how we have always done it” mentality.

- Support from Senior Management: At many organizations internal audit still doesn’t have the backing of senior management and the board to try new things, embrace advanced technologies, and challenge the status quo.

“The biggest thing that came back from respondents is that their lack of ability to find the talent is one of the things that is hindering them with technology adoption,” says Massey. “We continue to see a very tight employment market as it relates to audit.”

The IIA data supports Massey’s concerns. “Finding and attracting enough candidates with the right skills continues to be a challenge for many CAEs,” the report’s authors write. More than 90 percent of CAEs report difficulty in recruiting experienced personnel, and 60 percent express difficulty recruiting entry-level staff. Getting any talent, but especially experienced talent, is difficult, the study indicates. Most CAEs (72 percent) say they have gaps to fill in their assessment of needed skills.

Protiviti’s report also cites talent as a top roadblock to adopting technology, particularly in the area of advanced data analytics. “Internal audit groups continue to face a lack of skills in understanding and using analytics technologies,” says Christensen.

Another reason internal audit departments are slow to adopt new technology is complacency. All three reports say that internal audit needs to adopt a mindset of innovation to move past the technological myopia. “The tendency for some CAEs might be to wait for others to act first,” says the IIA report. “This is a recipe for irrelevance. CAEs need to position internal audit to be an internal disruptor, relentlessly challenging the status quo, identifying and focusing on emerging risks.”

The third major barrier to moving toward better and faster implementation of leading technologies is support from senior management and the board. According to the IIA report, 38 percent of CAEs responded that overly traditional expectations of executive management are a roadblock to agility. And Protiviti finds a clear correlation between the audit committee’s level of interest in the use of analytics to support the auditing lifecycle and the amount of information shared with the committee about the use of auditing analytics. Some 59 percent of respondents agreed that when a high level of information is shared with the audit committee, there is also a high level of interest from the audit committee in the use of audit analytics.

It’s important to note that barriers that were at the top of the list in the past, namely cost and complexity of technology, have slipped down the list. “CAEs should not consider more resources as the primary solution to a lack of innovation. Like agility, innovation requires a mindset change even more than resources. It only takes a few of the right people to produce a tremendous amount of innovation,” write the IIA report’s authors.

Embracing Technology Pays Dividends

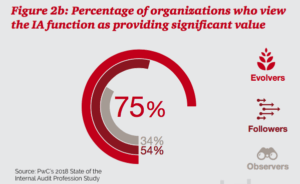

PwC finds that the technology adopting internal audit functions are more likely to be perceived by senior management and the board as adding significant value. “The business case for being an Evolver is strong. Evolvers are rated as more valuable to an organization, with 75 percent of them contributing significant value versus 54 percent of Followers and 34 percent of Observers,” the report’s authors write.

The PwC report highlights Evolver characteristics which make these top-performing Internal Audit functions stand out. These include:

- They move technology and talent in lockstep. Evolvers are advanced in their technology use and far outperform their peers on talent: 72 percent of Evolvers excel at obtaining, training and sourcing the talent they need compared to 46 percent of Followers and 29 percent of Observers.

- They build a deliberate strategy. 85 percent of Evolvers focus on technology enablement as part of their strategic plan, compared to 61 percent of Followers and 38 percent of Observers.

- They leverage technology-enabled collaboration tools. Internal Audit functions that are advanced in their use of collaboration tools stand out from their peers in managing stakeholder relationships and cost efficiencies.

- They are self-service in data extraction. More than 80 percent of Evolvers are self-sufficient in their data extraction.

- They utilize tools and skill sets for enhanced productivity. From advancing data analytics and monitoring, to leaning into intelligent automation, Evolvers are more often investing in technology risks and tools training than their peers.

“In order to keep pace with their organization’s innovation agenda, Internal Audit needs a strong technology and talent strategy to push the boundaries of their own innovation,” says Massey. “Internal Audit could have the best innovation plan, but won’t be able to execute without the right reinforcements. The combination of technology and talent is the key to accelerating progress,” she says.

How Do We Get There?

When it comes to how to advance internal audit’s adoption of technology, all three reports seem to indicate that internal audit is poised to overcome the tech challenge, but a shift in mindset and some heavy lifting will be required to get there.

This is also apparent in emerging markets particularly Asia amd the Middle East. Even professional firms providing IA and risk services are struggling to incorporate innovative technology which greatly affects value. Additionally, some ACs lack enthusiatic sponsorship to the adoption especially when IA’s performance is perceived to be poor (e.g. when IA is just introduced). This makes IA less exciting plus the fact that incumbents are sticking to the norm.

Technological advancement in IA is sophisticated and challenging as it can’t be done just like picking items off the shelves. Systems, infrastructure and culture are different from one organization to the other. Thus tailor-fitting is a necessity which can at times be costly. And, its relevance is a race with time as technology always evolve. What was adopted today may not be relevant tomorrow.

This makes me sad. IA is struggling as assurance does.

Thanks for your thoughtful and excellent comment. -Joe