As the vaccination effort continues and hope is spreading that we might be nearing the end of the COVID-19 pandemic, it’s still too early to assess the long-term impact the past year of crisis will have on daily life, the economy, and—as it relates here—the internal audit profession.

Now, a new survey looks to shed some light on the pandemic’s varied effects on organizations and internal audit. It’s still likely to be some time before offices are returning to normal, and internal auditors no longer face the challenges of conducting audits remotely and without the valued face-to-face interactions—apart from Zoom calls—with colleagues, audit clients, and others. One thing is clear, the Coronavirus Crisis has not impacted businesses uniformly. While some industries, such as travel, hospitality, and live entertainment, have been devastated, others, such as technologies that enable remote work, have thrived. Internal auditors in such industries have been pulled in different directions and have faced vastly different issues.

The survey, 2021 North American Pulse of Internal Audit: Many Sides of Crisis, published by the Institute of Internal Auditors, shows this disparity in the opportunities the pandemic has produced, as well as in the costs it has extracted. The pandemic’s effects on internal audit were noted across a broad spectrum of reliable Pulse survey metrics, including internal audit budgets, staffing, risk assessments, and audit plans.

An Opportunity for Internal Audit

While the pandemic’s impacts varied by industry, Pulse survey results consistently show that the effects on the internal audit function were less severe than for the organization as a whole. Among the most dramatic difference was within the health care and social assistance sector, where 80 percent of respondents from such organizations rated the pandemic’s impact as “extensive” for the overall organization, yet only 37 percent rated it as such for the internal audit function. In financial services and insurance, just 18 percent of respondents rated the pandemic’s impact as minimal for the overall organization, while more than twice as many (41 percent) rated it as minimal for the internal audit function itself.

“The pandemic created an open audition for internal audit to showcase its value, particularly in response to the crisis management and business continuity risks at the onset of the pandemic,” the report’s authors write. “Indeed, responses from CAEs who reported staffing increases support that, for some, pandemic responses expanded the profession’s scope of work. In aggregate, the pandemic’s impacts were less than initially anticipated by internal audit leaders.”

“Taken together, these trends suggest stakeholders may place a priority on internal audit providing assurance on financial and compliance risks, which can be perceived as essential in times of crisis,” The report states. “The need for internal audit expertise in these areas may have provided a backstop against even more significant reductions of internal audit budget and staffing.”

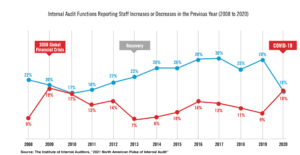

A Little Belt Tightening

In regard to budgets and staffing, the news was mixed. While more internal audit leaders reported cuts to budgets (36 percent) compared to those who said they experienced a budget increase (20 percent), the cuts were generally less than expected by CAEs. A June 2020 IIA survey found that 45 percent of audit leaders expected a budget cut, 9 percent more than those who actually did experience one. For many internal audit functions, budgets remained flat, with 44 percent of CAEs reporting no change to budgets. It’s true too, though, that more CAEs reported budget cuts than those reporting increases for the first time since 2009, ending 10 years of internal audit budgets generally increasing.

Not surprisingly, budget and staffing cuts were the most prevalent in industries hardest hit by the pandemic. For example, 58 percent of audit leaders in educational services reported cuts and 48 percent in consumer-facing businesses like retail and travel experienced a cut to budgets. Meanwhile, in financial services just 20 percent of CAEs reported cuts and 28 percent said their budgets increased. Public administration organizations noted similar results with cuts at 27 percent of respondents, while 24 percent said they got increases.

“How internal audit leaders chose to manage budget cuts also tells an important story,” the report states. “Notably, only 17 percent said they decreased the internal audit staffing budget and only 26 percent decreased the external sourcing budget. Slightly more (about one-third) said the budget for professional development decreased. The most widespread budget cuts were for travel (83 percent), a predictable outcome given the pandemic dramatically limited the ability of practitioners to travel.”

Risk Levels Rising

While it’s no surprise that audit leaders say risk levels are increasing, given the massive disruptions the pandemic has created, the situation might not be all that bad. Risk levels increased in most audit areas for public sector and nonprofit organizations. Fewer areas of increasing risk were reported, however, for publicly traded, financial services, and privately held organizations. Audit plan allocations reflected these areas of increased risk, including cybersecurity, third-party relationships, and compliance and regulatory issues. Data reflected increases in audit plan allocations for cybersecurity and financial reporting and declines for operational risks.

Audit plan trends suggest stakeholders may place a priority on internal audit providing assurance on financial and compliance risk activities, which can be perceived as essential in times of crisis. As noted in the report, risks relating to economic uncertainty, regulatory changes, and safely emerging from the pandemic should alert internal audit leaders to weighty challenges ahead.

“The need for internal audit expertise in these areas may have provided a backstop against even more significant reductions of internal audit budget and staffing,” according to the report. “The clear message from this year’s Pulse data can be summed up in the maxim: We are all in the same storm, but not the same boat.”

The IIA’s Audit Executive Center (AEC) has gathered insight from leaders in the profession through the annual Pulse of Internal Audit survey since 2009. Each survey collects information and perceptions from internal audit leadership, primarily chief audit executives (CAEs) and directors and senior managers of internal audit across the public, private, and nonprofit sectors.

Certainly, the pandemic has brought its fair share of change and disruption to internal audit functions, as the survey documents. How soon those circumstances begin to return to “normal,” if ever, is anybody’s guess. ![]()

![]()

Joseph McCafferty is editor & publisher of Internal Audit 360°.

One Reply to “New Survey Examines the Pandemic’s Impact on Internal Audit”